NHS capital flows

How much does the NHS spend on capital projects and where does this money come from?

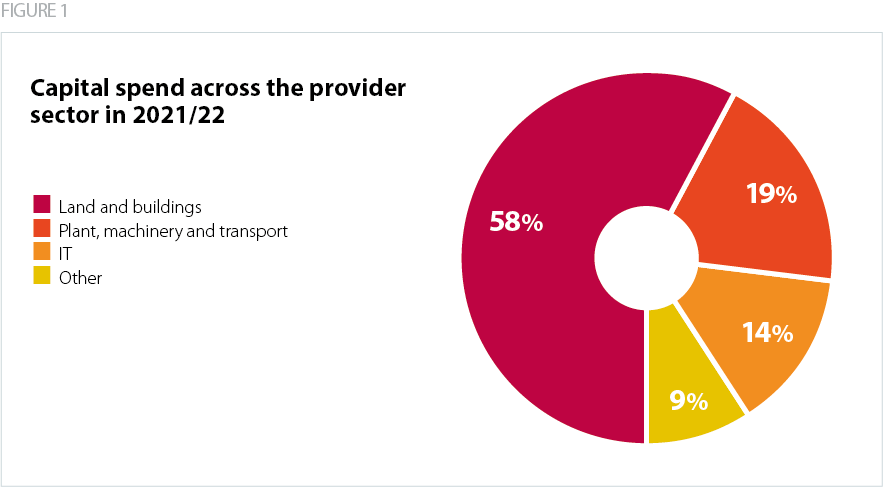

The Department of Health and Social Care’s (DHSC’s) capital budget is used to finance capital investment in the NHS. In 2021/22 NHS providers spent 75% of DHSC’s capital budget. Just over half of NHS capital expenditure covers land and buildings. The remaining proportion is used for plant, equipment and transport (which includes diagnostic equipment like MRI and CT scanners), and information technology.

The NHS capital regime is broadly split between operational capital and nationally allocated capital. Operational capital covers day-to-day investments such as maintenance renewal self-financed by trusts through retained surpluses or via loans from DHSC and public dividend capita (PDC). There are also nationally held capital funds which cover strategic projects like new hospitals and hospital upgrades. Other national capital investment includes elective recovery, diagnostics programmes, and digital funding.

The NHS has been unable to enter into new public private partnerships since 2018. Until that point these were a well-used financing route for major building programmes. Assets were financed via public finance initiative (PFI) providers who then leased them back to the public sector with contracts which often included estates and facilities management costs. However, these contracts carried significant annual unitary charges.

Raiding capital budgets to boost revenue

Following significant cuts in public spending, the NHS capital budget was raided between 2014/15 and 2018/19 as DHSC prioritised day-to-day spending at the expense of vital long-term investment. In the short term it was easier to cut investment than day-to-day spending. During this period DHSC transferred £4.3bn from the capital budget into the revenue pot.

As The Health Foundation has shown, had the UK matched EU14 levels of capital spending as a share of GDP it would have invested £33bn more in health-related assets between 2010-2019. 7 This would have amounted to a 55% uplift against actual health capital spending during this period.

The relative lack of capital investment limited the scope for productivity improvements. As the long-term plan highlighted, the NHS uses its assets and infrastructure more intensively than equivalent health economies. The Health Foundation notes the 'capital thinning' across the NHS over the last decade, whereby capital per worker fell – this is a proxy measure used to assess overall capital investment levels. Given trusts have been using their infrastructure and equipment for longer – which meant the value of their assets depreciated less each year – the value of capital increased only marginally between 2010/11 and 2017/18.

Current levels of capital investment

Recent capital announcements represent a major uplift to the NHS capital budget

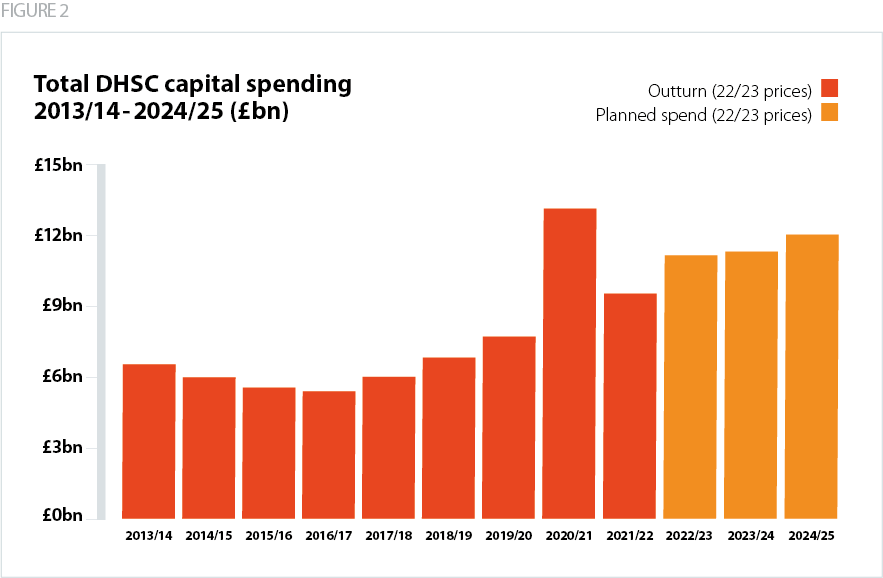

There has been major growth in DHSC’s capital budget over recent years. This has resulted in a substantial increase in capital allocations across the provider sector. Capital investment across the NHS over the current Spending Review (SR) period (2022/23 - 2024/25) is expected to average £8bn per annum, whereas annual capital spending averaged £3bn between 2010-19.

Sources: NHS Providers analysis of HM Treasury data using December 2022 GDP deflators – HM Treasury: ‘Public Expenditure Statistical Analyses 2022’, July 2022; ‘Autumn Statement 2022’, November 2022; ‘Supplementary Estimates 2022-23’. February 2023; ‘December 2022 GDP deflator series’, November 2022. Office for Budgetary Responsibility, ‘November 2022 GDP deflator forecasts’, November 2022. The capital profile for 2022/23-2024/25 appears higher than outlined at the October 2021 Spending Review due to the reclassification of leases as part of the IFRS16 accounting standards.

Trusts welcomed the multi-year capital budget set at the October 2021 SR. This was the first multi-year settlement since 2015, and providers have since been given indicative capital allocations for 2023/24 and 2024/25. After years of underinvestment, the capital settlement has given trusts and systems greater certainty for medium-term financial planning.

The government expects to allocate £12bn over the SR period for maintenance and improvements across the estate. For 2023/24, NHSE has allotted £4.1bn to operational capital envelopes and £3.6bn to nationally allocated funds and other national capital investment.

As section four highlights, this increase included nationally allocated capital to support elective waiting list recovery, improve digital technology, transform diagnostic services, create new surgical hubs, expand bed capacity and improve equipment. This investment was largely targeted at hospital settings.

Inflationary pressures and the medium-term outlook for health capital spending are concerning

In the Autumn Statement the government confirmed that departmental capital budgets announced at the SR would remain the same at flat cash levels. However, given the current and anticipated level of inflationary pressures over the remainder of the SR period, the cash settlement is forecast to decrease in real terms.

After 2024/25, the Office for Budget Responsibility (OBR) forecasts that the government’s total capital envelope will fall by 1.2% in real terms per annum rather than increasing at the same level of nominal GDP growth. CDEL spending will fall to 3.3% of GDP in 2027/28, thereby reversing half of the March 2020 Budget uplift.

Inflation is limiting trusts’ capacity to deliver capital projects within initial cost estimates. In some cases, trusts are delaying (or abandoning) projects because costs have spiralled; others are rephasing and rescaling planned works. There are also capacity and capability issues affecting delivery. While construction price inflation has somewhat stabilised, supply chains remain constrained and input cost inflation – impacting labour and materials – is leading to higher costs over the SR period. Inflation will ultimately eat away at the nominal capital settlement.